IRA Compliance Software for the 5x Bonus Credit.

DSPTCH is real-time IRA prevailing wage and apprenticeship compliance software. Calculate per-worker obligations before payroll runs, track daily apprentice ratios, generate WH-347s in one click, and see live Cure Provision penalty exposure before the credit is at risk.

The Three Pillars of IRA Compliance

The Inflation Reduction Act ties a 5x credit multiplier to two requirements: prevailing wage and apprenticeship. Failing either reduces the credit by 80% unless cured under the 26 CFR 1.45-7 and 1.45-8 correction framework. Here's how each piece works.

Pay Davis-Bacon Rates to Every Laborer and Mechanic

All laborers and mechanics performing covered construction, alteration, or repair on an IRA-qualified project must be paid no less than the applicable federal prevailing wage and fringe rate published by the U.S. Department of Labor. The obligation flows to every contractor and subcontractor at every tier.

• Continues through the alteration and repair window (5 yrs for ITC, 10 yrs for PTC)

• Scope governed by Davis-Bacon classifications and DOL conformance under 29 CFR 5.5

Hit the Labor Hours, Ratio, and Participation Tests

IRA apprenticeship compliance has three components that operate independently. Each one must be satisfied, every day, for every contractor on covered work.

• Labor Hours: 15% of total construction labor hours from qualified apprentices (12.5% for 2023 BOC

• Daily Ratio: apprentice-to-journeyworker ratio set by the registered program, tested every day on site

• Participation: any contractor with 4+ workers on covered work must employ at least one qualified apprentice

Cure Inside the Window. Keep Audit-Ready Records.

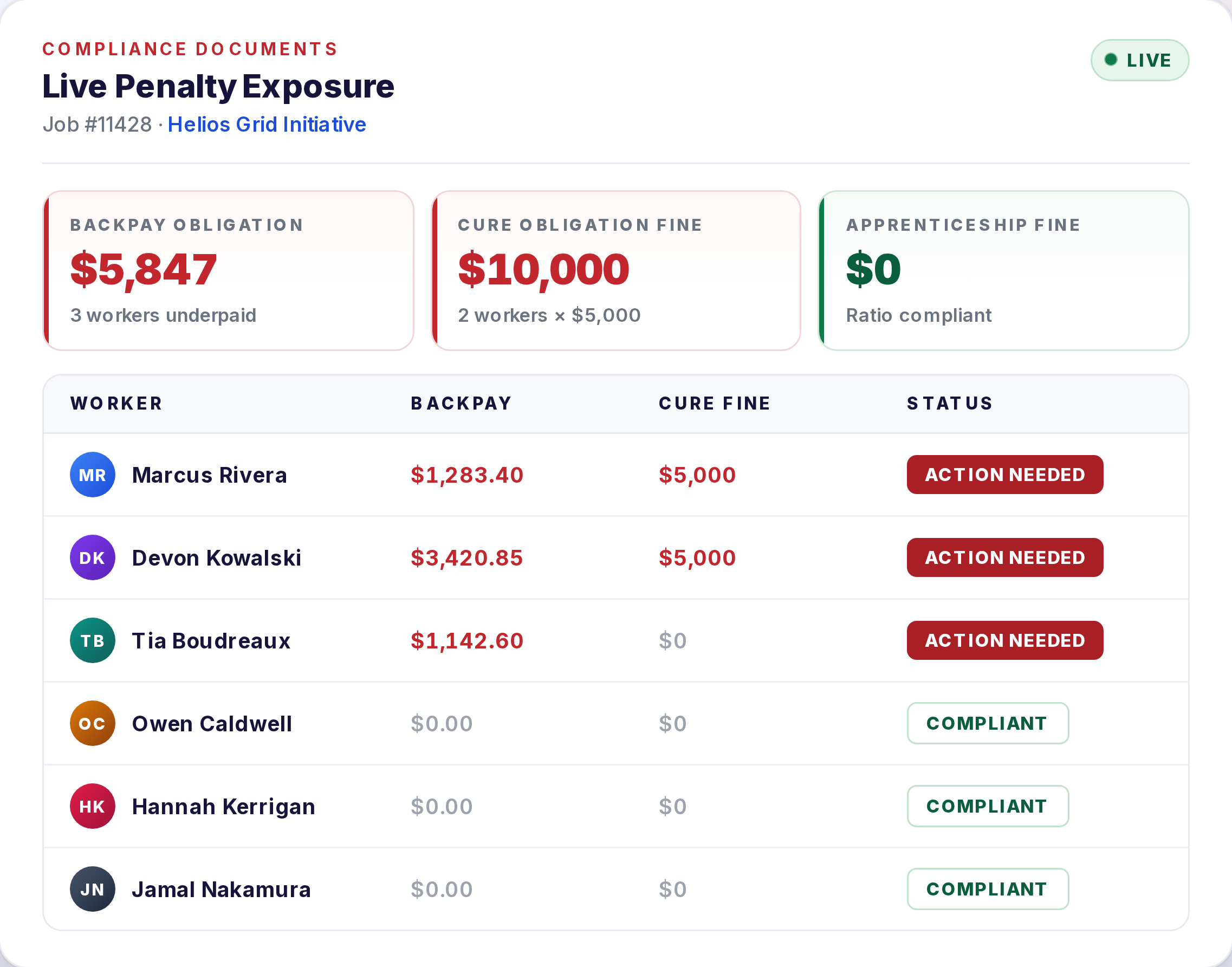

Treasury's correction framework (26 CFR 1.45-7 and 1.45-8) lets taxpayers preserve the 5x credit by paying backpay, interest at section 6621 plus 6 points, and per-worker penalties to the IRS. Records must hold up across the six-year statute of limitations and the 5-year recapture window for ITC-type credits.

• 3x backpay multiplier and $10,000 per worker if intentional disregard applies

• Good Faith Effort exception under 26 CFR 1.45-8(f) requires 5-business-day denial documentation

prevailing wage corrections

PWA Compliance, Two Ways.

Whether you’re an asset owner overseeing contractors or a contractor running your own crews, DSPTCH covers PWA compliance end to end.

Prevailing Wage Compliance, Handled for You

You don’t need to manage compliance. Just make an introduction, and we take it from there.

- One intro email does it all. We onboard every contractor and sub directly.

- Full visibility, anytime. Wages, ratios, and certifications for every contractor, 24/7.

- Issues handled before they become costly. Get notified the moment a contractor goes out of ratio or underpays so corrections happen inside the 180-day window

- Recapture-grade records. Wages, ratios, and certifications for every contractor, retained for the 6-year SOL and 5-year recapture window

PWA Compliance for Your Self-Perform Work

Know what you owe before payroll runs, not six weeks later.

- Prevailing wage obligations calculated before payroll closes, not after

- Hours flow into PW calculations with eligible and ineligible hours separated automatically

- Apprenticeship ratios tracked in real time

- 200+ payroll integrations move your data each period. No spreadsheets, no re-keying.

IRA Compliance Resources

Start with the comprehensive Field Guide, or jump to a topic-specific one-pager. Both are written for compliance leads, EPCs, and tax-credit project sponsors.

The DSPTCH IRA Field Guide

The full operator's manual for IRA Prevailing Wage & Apprenticeship compliance. Applicability, scope of work, apprenticeship math, the Good Faith Effort safe harbor, the 26 CFR 1.45-7 / 1.45-8 cure framework, and every penalty line item in one document.

Quick references on individual IRA topics

IRA Prevailing Wage & Apprenticeship Applicability

Confirm whether the PWA regime applies to a project before pricing the credit, including the One Megawatt and pre-2023 BOC exceptions.

View One Pager →

Scope of WorkIRA Prevailing Wage Scope of Work Eligibility

Which laborers, mechanics, and site activities are inside Davis-Bacon scope under the IRA, including secondary-site rules and conformance.

View One Pager →

ApprenticeshipIRA Apprenticeship Requirements

The labor hours, daily ratio, and participation tests that drive apprenticeship compliance under sections 30C, 45, 45Q, 45V, 45Y, 45Z, 48, 48C, 48E, and 179D.

View One Pager →

Out of Ratio ApprenticesApprentices Out of Ratio

What happens when the daily ratio is exceeded: how excess hours fail the 15% test and trigger prevailing-wage underpayments simultaneously.

View One Pager →

Good Faith Effort ExemptionIRA Good Faith Effort Exception

How to rely on 26 CFR 1.45-8(f), including the 5-business-day denial standard, the 365-day renewal cycle, and documentation requirements.

View One Pager →

PenaltiesIRA Prevailing Wage Penalties

The $5,000 per-worker IRS penalty, intentional-disregard 3x backpay multiplier ($10,000), and Section 6621 interest math.

View One Pager →

Cure FrameworkIRA Cure & Penalty Correction Framework

26 CFR 1.45-7 and 1.45-8 step-by-step: the 180-day window for PW, the $50 per labor-hour apprentice penalty, and recapture risk inside the 5-year window.

View One Pager →

Fringe BenefitsIRA Prevailing Wage Fringe Benefits

What counts as a bona fide fringe under 40 U.S.C. 3141 and 29 CFR Part 5, the 29 CFR 5.25(c) annualization formula across 2,080 annual hours, and the records the IRS expects under 26 CFR 1.45-12.

View One Pager →

See DSPTCH

in action.

Book a 30-minute demo. See how DSPTCH gives your team a real-time view of every pay period, from field capture to certified payroll handoff.

Book a demo

Fill out the form and we’ll reach out within one business day.

IRA Compliance FAQ

Common questions on IRA prevailing wage, apprenticeship, penalties, and the 5x bonus credit.

What is IRA compliance?

IRA compliance refers to meeting the prevailing wage and apprenticeship (PWA) requirements introduced by the Inflation Reduction Act for ten clean-energy tax credits and deductions (IRC sections 30C, 45, 45Q, 45V, 45Y, 45Z, 48, 48C, 48E, and 179D). Meeting both PWA requirements multiplies the base credit by 5x. Failing either reduces the credit by 80% unless cured through Treasury's correction framework in 26 CFR 1.45-7 and 26 CFR 1.45-8.

Which IRA tax credits require PWA compliance?

The PWA requirements apply to ten clean-energy credits and deductions: section 30C (alternative fuel refueling property), 45 (production tax credit), 45Q (carbon capture), 45V (clean hydrogen), 45Y (clean electricity PTC), 45Z (clean fuel production), 48 (investment tax credit), 48C (qualifying advanced energy), 48E (clean electricity ITC), and 179D (energy-efficient commercial buildings). Sections 45L and 45U have no apprenticeship requirement.

What is the IRA 5x bonus credit?

Most IRA clean-energy credits start at a base rate (often 6% for the investment tax credit) and are multiplied by 5 when the taxpayer satisfies both the prevailing wage requirement and the apprenticeship requirement during covered construction, alteration, or repair work. Missing PWA cuts the credit to the base rate, an 80% reduction in credit value.

What is the One Megawatt Exception?

Projects with a maximum net output of less than one megawatt (AC) are exempt from the IRA prevailing wage and apprenticeship requirements and still qualify for the full 5x credit. The exception is project-by-project and does not apply to all credit sections. For 45V clean hydrogen, a different threshold applies.

What is the Beginning of Construction (BOC) exception?

Projects that began construction before January 29, 2023 are grandfathered out of the IRA PWA requirements entirely and still qualify for the 5x credit. Beginning of construction is established through the Physical Work Test or the Five Percent Safe Harbor, with continuity requirements that follow the same standards used for the prior PTC and ITC.

What are the IRA prevailing wage requirements?

All laborers and mechanics performing construction, alteration, or repair on a covered IRA project must be paid no less than the applicable Davis-Bacon prevailing wage and fringe rate published by the U.S. Department of Labor for the project's locality and classification. The obligation extends to contractors and subcontractors at any tier and continues through the alteration and repair period (5 years for ITC-type credits, 10 years for PTC-type credits).

What are the IRA apprenticeship requirements?

IRA apprenticeship compliance has three components. Labor Hours: qualified apprentices must perform at least 15% of total construction labor hours for projects starting construction in 2024 or later (12.5% for 2023 starts). Daily Ratio: the apprentice-to-journeyworker ratio set by the registered apprenticeship program must be met every day on site, in every occupation. Participation: any taxpayer, contractor, or subcontractor employing four or more individuals on covered work must employ at least one qualified apprentice.

How is the IRA Cure Provision penalty calculated?

For prevailing wage failures, the taxpayer pays each underpaid worker the wage shortfall plus interest at the section 6621 underpayment rate with 6 points added, plus a $5,000 per-worker penalty to the IRS ($10,000 per worker with a 3x backpay multiplier for intentional disregard). For apprenticeship failures, the penalty is $50 per deficient labor hour ($500 per hour for intentional disregard). Prevailing wage corrections have a 180-day deadline after IRS final determination.

What is the IRA Good Faith Effort exception?

Under 26 CFR 1.45-8(f)(1), a taxpayer is deemed to satisfy the IRA apprenticeship labor-hours and ratio requirements when qualified apprentices were properly requested from a registered apprenticeship program and the request was either denied or not substantively answered within 5 business days, so long as the denial was not caused by the taxpayer's refusal to comply with program standards. Requests must be renewed every 365 days while construction continues.

What records do contractors need to keep for IRA compliance?

Treasury requires audit-ready recordkeeping for the full statute of limitations period (generally six years). Required records include weekly certified payroll (WH-347), wage determinations by classification, daily apprenticeship ratio logs, apprentice registration documentation, good faith effort requests and responses, and worker classification support. Records must be retained for the taxpayer, every contractor, and every subcontractor at every tier.

What happens if work is outside the wage determination scope?

Work outside published Davis-Bacon scopes requires a conformance request to the U.S. Department of Labor under 29 CFR 5.5(a)(1)(ii). Until DOL approves a conformance, paying the wrong rate creates prevailing wage underpayments that must be cured. Site-of-work boundaries also matter: work at a secondary site dedicated to the IRA project is generally covered, while work at a commercial supply yard generally is not.

How does DSPTCH help with IRA compliance?

DSPTCH is IRA compliance software that calculates per-worker prevailing wage obligations before payroll closes, tracks daily apprentice-to-journeyworker ratios and the 15% labor-hours threshold in real time, auto-generates WH-347 certified payroll from 200+ payroll integrations, and shows live Cure Provision penalty exposure across every project. Asset owners get one view across every contractor; contractors catch issues inside the cure window instead of months later.

Who is responsible for IRA compliance, developer or contractor?

The taxpayer claiming the IRA credit is ultimately responsible to the IRS. That's typically the developer, asset owner, or tax-equity investor. But every contractor and subcontractor performing covered work at every tier must meet the prevailing wage and apprenticeship requirements. In practice, most asset owners flow the compliance obligation down through EPC and subcontractor agreements, and rely on real-time visibility to confirm contractors are actually meeting the requirements.

When did the IRA prevailing wage and apprenticeship rules take effect?

The IRA prevailing wage and apprenticeship requirements took effect for projects that began construction on or after January 29, 2023. Projects with a documented Beginning of Construction before that date are grandfathered out and still qualify for the 5x credit without meeting PWA. Treasury's final regulations (T.D. 9998) were issued on June 25, 2024.

Does IRA prevailing wage apply to O&M and maintenance work?

Yes, in many cases. The IRA prevailing wage requirement extends through the alteration and repair period after a facility is placed in service: 5 years for ITC-type credits under sections 48 and 48E, and 10 years for PTC-type credits under sections 45 and 45Y. Routine inspection and minor servicing are generally excluded, but substantive alteration or repair work performed during these windows is covered and requires Davis-Bacon wages.

What's the difference between Davis-Bacon and IRA prevailing wage?

Davis-Bacon is a federal contracting framework enforced by the U.S. Department of Labor on direct federal construction projects. IRA prevailing wage borrows the Davis-Bacon wage determinations, classifications, and scope-of-work concepts but is a tax-credit preservation regime, not a labor enforcement regime. Penalties under the IRA are paid to the IRS, not the DOL, and the goal is preserving the 5x bonus credit rather than satisfying a federal contract.

What is a qualified apprentice under the IRA?

A qualified apprentice is an individual enrolled in a registered apprenticeship program under the National Apprenticeship Act (29 USC 50), performing covered construction, alteration, or repair work on an IRA-qualified facility. The program must be registered with the U.S. Department of Labor's Office of Apprenticeship or a recognized State Apprenticeship Agency. Pre-apprentices and workers in unregistered training programs do not count toward the 15% labor-hours requirement or the daily ratio.

What's the difference between the IRA PTC and ITC?

The Production Tax Credit (PTC) under section 45 (legacy) and section 45Y (post-2024) pays a per-kWh credit over the first 10 years of operation. The Investment Tax Credit (ITC) under section 48 (legacy) and section 48E (post-2024) is a one-time credit calculated as a percentage of qualified project cost in the year placed in service. Both credits multiply by 5x when prevailing wage and apprenticeship requirements are satisfied, and both can lose the multiplier if PWA fails without cure.

What is the IRA recapture period?

For investment-type credits under sections 48 and 48E, there is a 5-year recapture window after the facility is placed in service. If prevailing wage or apprenticeship compliance fails during the alteration and repair window and is not cured, the IRS can recapture the 5x bonus portion of the credit already claimed. Production tax credits under sections 45 and 45Y have a 10-year alteration and repair window but no equivalent recapture mechanism, since the credit is earned year by year.

Does IRA compliance apply to wind, battery storage, and EV charging?

Yes. The prevailing wage and apprenticeship requirements apply to facilities claiming the 5x bonus credit under any of the covered sections: 30C (alternative fuel and EV refueling), 45 and 45Y (PTC for wind, solar, geothermal, and other generation), 45Q (carbon capture and sequestration), 45V (clean hydrogen), 45Z (clean fuel production), 48 and 48E (ITC for solar, wind, battery storage, and more), 48C (qualifying advanced energy manufacturing), and 179D (energy-efficient commercial buildings).

Are fringe benefits included in IRA prevailing wage?

Yes. Each DOL wage determination publishes both a base hourly rate and a fringe benefit rate per classification. The IRA prevailing wage obligation is the sum of the two. Contractors can satisfy the fringe portion by paying bona-fide benefits (health insurance, retirement contributions, paid leave) or by paying the fringe amount as additional cash wages. Mis-tracking the fringe component is one of the most common sources of IRA underpayments.

How do IRA tax credit transfers affect compliance?

Section 6418 allows clean energy tax credits to be sold or transferred to unrelated buyers. The compliance obligation, including prevailing wage and apprenticeship, stays with the project and the original taxpayer. Buyers inherit the risk that PWA failures could reduce or recapture the transferred credit, which is why credit buyers, lenders, and tax-equity investors increasingly require real-time PWA compliance evidence and software-backed recordkeeping as a closing condition.

Still have questions about IRA compliance? We'd love to walk you through it.

Book a Demo